Why don’t founders always choose the highest bidder? Why does preparation matter more than price in founder-led deals?

When a B2B software founder was evaluating which investor to partner with for the company’s next growth phase, valuation was not what made one party stand out.

What he remembered was preparation.

One investor entered the management meeting with a concrete view on the business. They had already thought through which new verticals the company could enter, which growth levers were still underexplored, and how to scale. They had not waited for the founder to explain the strategy. They had already formed one.

At the end of the session, the founder did not thank them for their offer. He thanked them for their preparation.

For this founder, the question was not simply who would pay the most. It was those who understood the business well enough to help build the next chapter.

As one internal KooKoo reflection put it:

“When someone walks in already knowing your strategic blind spots, not just your financials, it changes the dynamic entirely.”

That is the real point in many founder-led deals. Preparation is not just a good process. It is positioning.

Founder confidence is built before the final bid

In founder-led M&A, price matters. But it is rarely the only decision factor.

For many founders, a sale is not just a financial event. It is the handover of a company they built over the years: the team they hired, the customers they won, the culture they shaped, and the reputation attached to their name.

That is why founders often evaluate buyers through a broader lens.

They ask:

Who sees where the business can go next?

Who will protect the team and culture?

Who can help us scale without breaking what already works?

Who do I trust with the next chapter?

These questions are not answered in the final bid letter. They are answered much earlier, in every interaction before and during the process.

What do buyers often underestimate?

Many buyers invest heavily in the model, but less in the story they bring to the founder.

That is a missed opportunity.

In founder-led deals, the founder is not only evaluating the ,valuation. They are evaluating the buyer’s understanding, credibility and ability to create value after closing.

In some cases, price can even create new concerns. A stretched valuation may signal future pressure. A bold growth plan may sound attractive, but if it feels unrealistic, it creates doubt. Promises about continuity, autonomy, or culture lose credibility if they are not backed by a clear plan.

Founders can usually tell the difference between a buyer who is trying to win a process and a buyer who has genuinely understood the business.

Minority and majority deals require different positioning

Founder Decision Funnel. Kookoo Strategy

Deal structure also changes how founders think.

In a minority investment, the founder may see the investor as a growth partner. The emotional risk is often lower because the founder keeps influence, continuity, and upside.

In a majority acquisition, the concerns are different. The founder may worry about loss of control, cultural disruption, reduced voice, or a shift in identity. Even when the economics are attractive, these concerns can create resistance if they are not addressed early.

This means buyers cannot use the same message in every process.

A minority investor needs to show how they will support growth without taking over the founder’s role.

A majority buyer needs to show how they will protect what made the business valuable while still bringing the capabilities needed for the next phase.

The question is not only: “What is the offer?”

It is also: “What will this company become under this owner?”

Deal structure matters more than many buyers assume.

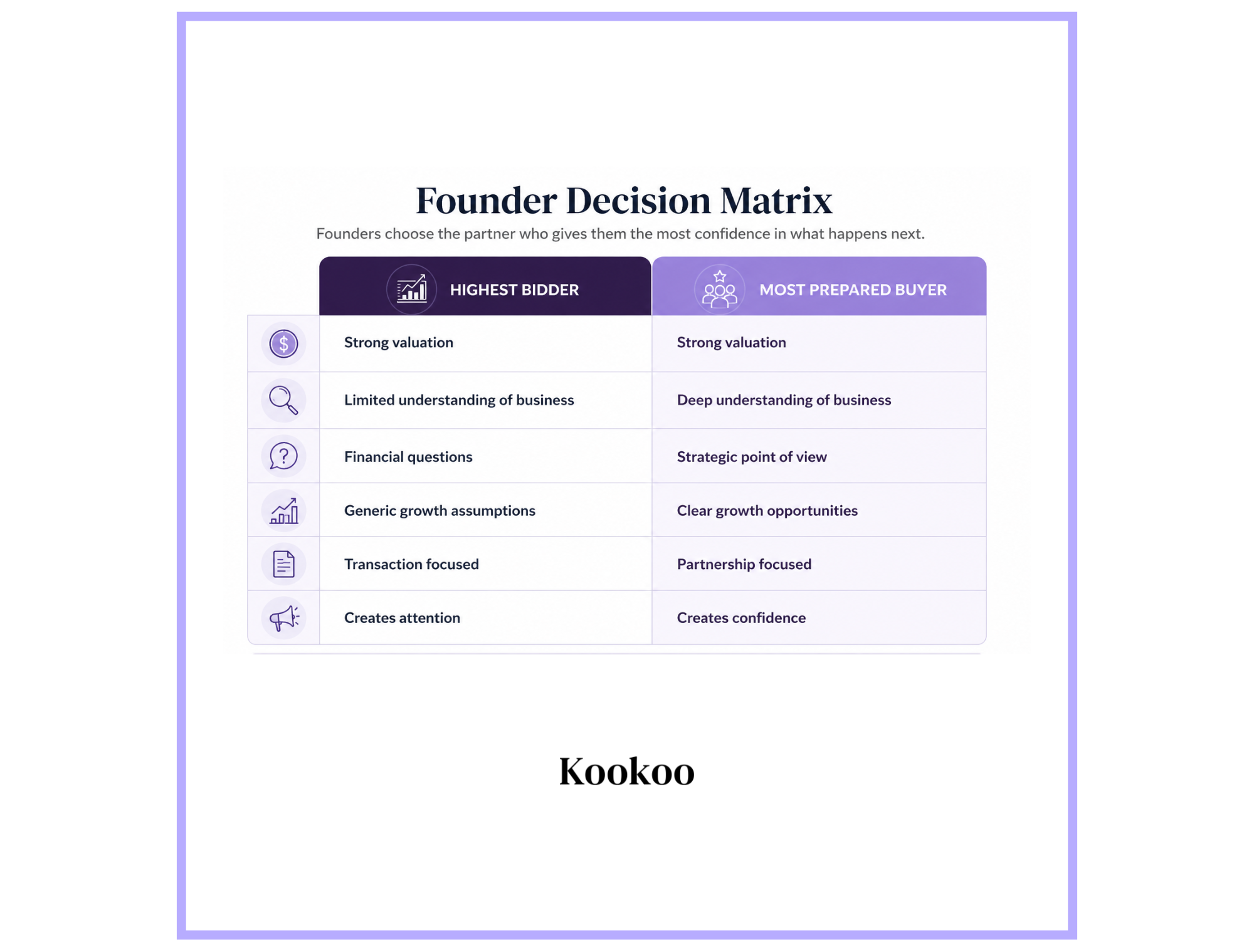

Founder Decision Matrix. Kookoo Strategy

Even when the economics are attractive, the majority deal can create psychological resistance if these concerns are not addressed early.

The lesson is clear: founders do not only assess valuation. They assess what control means after closing.

What do winning buyers do differently?

Winning buyers do not rely on price as their only differentiator.

They bring a point of view. They do not only ask what the company wants to do next. They show where they believe the next growth opportunities may be.

They reduce uncertainty. They make the founder feel that the next chapter is clearer, not riskier.

They respect what has already been built. They understand that people, culture, customers, and reputation are part of the deal.

They position themselves early. They build credibility before price becomes the only visible comparison point.

This is why preparation can become a source of competitive advantage. It helps the buyer move from being another bidder to becoming the most credible future partner.

Where KooKoo comes in

At KooKoo, we help investors compete on more than valuation.

Our role is to help buyers enter founder-led processes with a sharper commercial point of view. That means understanding the market, identifying credible growth levers, pressure testing the value creation story, and translating it into a narrative that matters to founders and management teams.

Because in many deals, conviction is built before the final bid.

That is why commercial preparation matters. It helps investors show not only what they are willing to pay, but why they are the right owner or partner for the next phase of growth.

Looking to win founder-led deals without relying only on price? KooKoo helps investors sharpen their positioning, build founder conviction, and compete on more than valuation.