Exit readiness in private equity: Why preparation directly increases your multiple.

Most private equity exits are not determined in the final months of a sale process, yet companies' preparation for those exits often begins only then.

We have noticed that exit preparation often starts once advisors are appointed and the formal transaction process begins. At that stage, management teams assemble the data room, refine the equity story, and prepare for buyer diligence. However, by this point, many of the factors that ultimately shape valuation have already been established.

With growth targets already clear, operational performance can’t be pushed much further in those last months, and commercial risks are hard to change.

As a result, the process shifts from telling a value creation story to defending it under due diligence scrutiny.

The cost of late exit preparation

When exit preparation starts late, the workload becomes highly concentrated in the final months before a transaction.

Management teams rush to consolidate data, explain financial bridges, and validate commercial assumptions. At the same time, buyers apply increasing analytical pressure through diligence.

This dynamic rarely causes transactions to fail. More often, it affects how buyers price risk.

During diligence, investors frequently encounter issues such as:

Equity stories that are compelling but have insufficient data support.

Financial adjustments that require additional clarification.

Customer concentration risks appear larger than expected.

Operational processes that rely heavily on specific individuals.

Individually, these issues may not materially change the underlying quality of the business. Collectively, however, they can influence buyer confidence and negotiating leverage.

The result is familiar across many processes: valuation pressure, more conservative deal structures, and additional protections such as earnouts or escrow mechanisms.

In these situations, value is not necessarily lost because the business underperformed. It is often lost because preparation began too late to address structural questions before the sale process started.

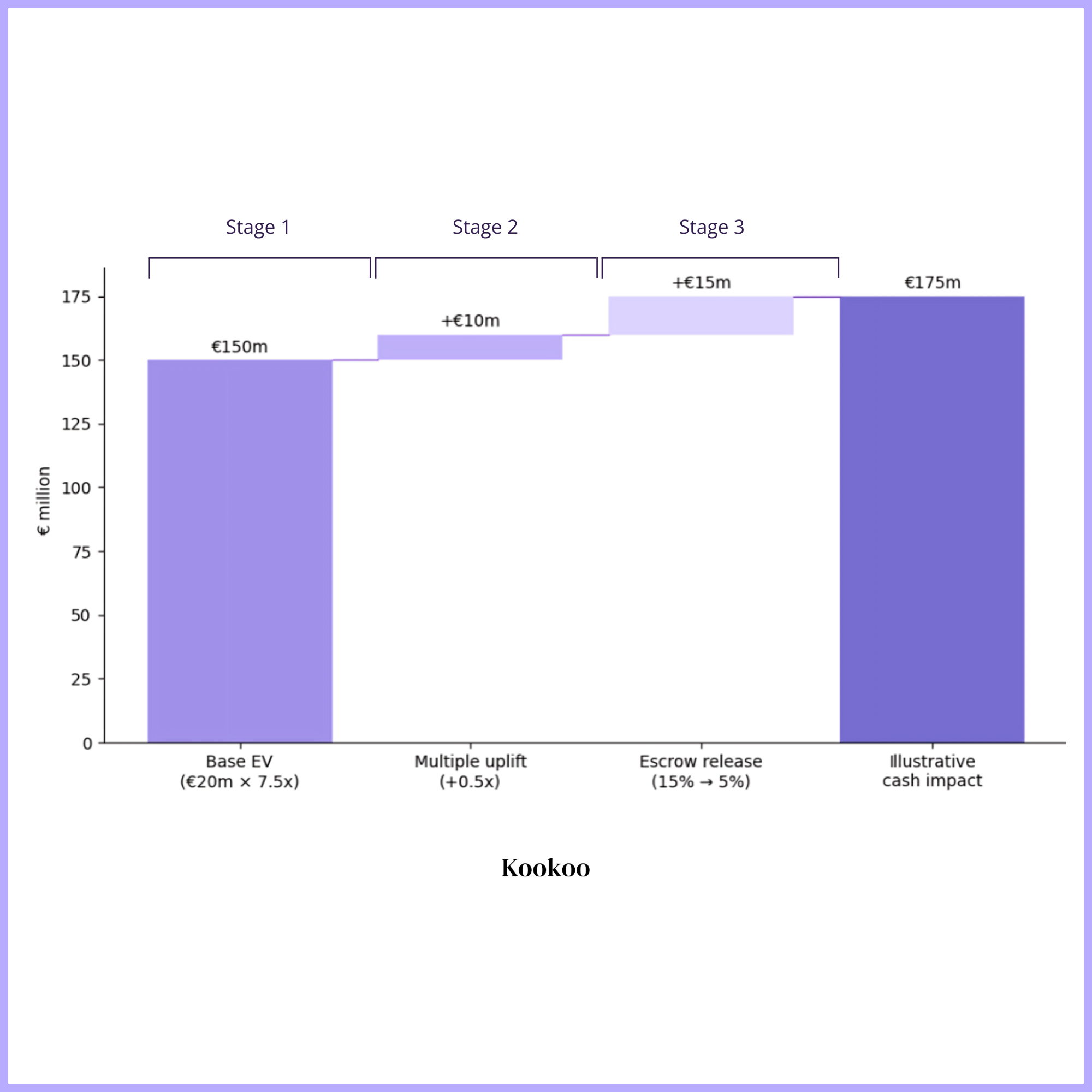

Enterprise value is typically shaped by three levers: EBITDA improvement through operational value creation, multiple expansion driven by buyer confidence and scalability, and certainty through a smoother close with less risk of retrade.

Value Capturing Strategy. Kookoo Strategy

Seen in the figure above with an example, starting from a base enterprise value of €150 million (stage 1), proactive preparation can expand the valuation multiple from 7.5x to 8.0x, adding €10 million in stage 2. By reducing deal risk, the portion of the price typically held in escrow to cover potential post-closing adjustments can drop from 15% to 5%, releasing an additional €15 million in cash at closing (stage 3). This demonstrates how early, strategic value creation directly increases both sale value and immediate cash proceeds.

Why should the preparation window begin earlier?

The most effective moment to prepare for an exit is typically well before the transaction process begins. In practice, many investors find that the critical preparation window begins approximately two years before a potential exit.

At this stage, business leaders still have time to influence structural drivers of valuation rather than simply documenting them. Examples include:

Strengthening the equity story with data-driven analysis

Reducing customer or revenue concentration risks

Institutionalizing data collection, financial reporting and KPI transparency

Demonstrating operational scalability to future buyers

Clarifying governance structures and management depth

These improvements cannot be implemented in the final months before a sale. They require operational change and measurable evidence over time.

The relevance for companies held for three to four years

For many private equity portfolios, this preparation window emerges when companies have been held for approximately three to four years.

At that point, investors often begin considering potential exit timing. However, many of the questions buyers will eventually raise during diligence have not yet been systematically assessed. Examples include:

Is the equity story supported by sufficient quantitative evidence?

Would financial reporting withstand detailed buyer scrutiny?

Are commercial dependencies clearly understood and mitigated?

Is the management structure scalable to the next phase of ownership?

Addressing these questions early provides investors with time to strengthen the business before the exit process begins.

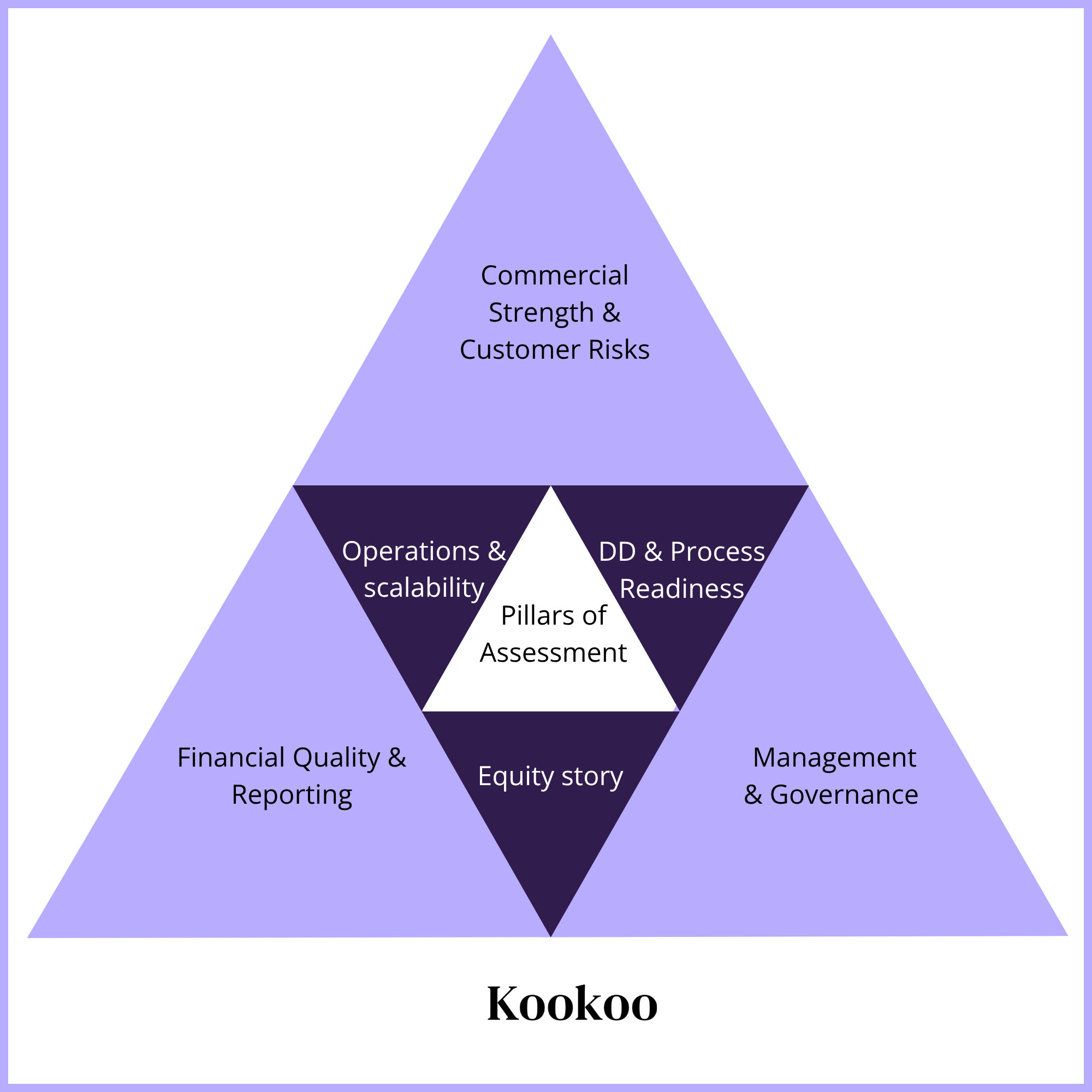

A diagnostic perspective on exit readiness

To explore how prepared portfolio companies are for this stage, we recently developed a short exit readiness diagnostic survey designed for private equity investors and their management teams.

The survey evaluates several dimensions that frequently influence buyer perception during diligence, including:

Pillars of Assessment. Kookoo Strategy

The goal is not to predict exit outcomes, but to provide an early perspective on how a business might appear through a buyer’s lens.

One recurring observation in similar diagnostics is the difference in perception between investment teams and management teams. In many cases, both believe the business is well prepared, yet their assessments diverge on specific risks or priorities. Identifying these differences early can help investors focus improvement efforts before the transaction process begins.

What differentiates our approach is the combination of management and investor perspectives, allowing us to identify not only gaps but also misalignments that typically surface during due diligence.

Key Insight: Most value loss in private equity exits stems not from performance, but from late preparation, misalignment, and insufficient evidence. Starting exit readiness early strengthens the equity story, reduces risk, and boosts both valuation and cash proceeds.

An invitation to participate in a pilot

We are currently inviting a small group of private equity firms to participate in a pilot of this exit readiness survey.

The focus is on investment managers responsible for portfolio companies that have been held for three to four years, where strategic preparation for exit often begins.

The survey requires approximately 30 minutes to complete and provides an early diagnostic view of potential preparation gaps and valuation risks.

Participation is limited, with a few additional spots reserved through trusted introductions.